If you end up finding this informative, a restack helps it reach more people. Enjoy!

I have good news, and I have bad news. Potentially really bad news. But first, the good news.

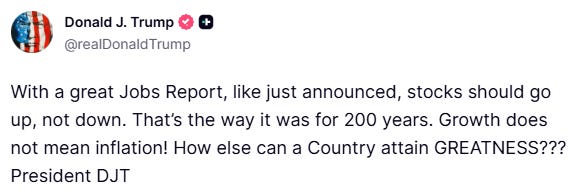

Last Friday, the US reportedly added 172,000 jobs in May, beating the consensus forecast of about 60,000-100,000 by a wide margin — with Olu Sonola, head of US economics at Fitch Ratings telling the Financial Times that “this is a blowout jobs report.”

Now the bad news. Shortly, after the Nasdaq 100 — the index tracking the biggest US-tech stocks — dropped by a whopping 4,7 percent in a single day. For context, a drop of 10 percent constitutes a correction.

Even the GREATEST truther-in-chief is confused:

Let me walk you through it.

By the end of this, you’ll understand the machine keeping the US economy alive better than most of the financial journalists paid to explain it. This includes a few things they’d rather you didn’t know. And you’ll see why there are now only two ways this ends, both of them ugly.

Answering Donald Trump’s confusion

A strong jobs report means that the economy is performing better than expected. Fewer people who are homeless (crude, yes — but that is essentially what “strong employment” means in America) means more inflation, because they are spending money on… Well, necessities.

This in turn means that the Federal Reserve is more likely to raise interest rates, raising the cost of borrowing.

And who is borrowing a lot right now?

You guessed it: AI-companies. They have borrowed roughly $121 billion over the course of 2025 — more than four times their usual pace. Morgan Stanley expects the hyperscalers and their joint ventures to issue $250-300 billion in debt in 2026 alone, and JPMorgan estimates the sector may need to raise as much as $1.5 trillion in investment-grade bonds over the next five years.

And I wish the bit about homeless people was just a joke. It’s not. The fact that such a positive number is followed by such negative reactions in the stock market, is in my view, the proof in the pudding that the US economy is severely sick, and is at least in part running on hot air.

While AI is a revolutionary technology, it is becoming clearer and clearer to citizens and capitalists alike that the costs outweigh the benefits, for different reasons.

The bottom 25-601 percent of Americans are living paycheck to paycheck and look over to the richer and flourishing side of town, where the top 10 percent who own 90 percent of the financial assets live — they currently account for a whopping 49.2 percent of consumer spending. They don’t feel the effects of AI-data centers increasing their energy bills and they don’t see the grass turning brown due to water shortages; matter of fact, when they open their Robinhood account all they see is green.

Simultaneously, in Manhattan and Silicon Valley offices, capitalists are looking at how much of their bottom line is going to Claude now that it has revealed its actual token rates, and are going: “yikes….”

So, to summarise what is keeping the economy afloat: wealthy Americans, buoyed by rising stock portfolios, are sustaining demand; poorer Americans are barely scraping by, but the economy is just performing well enough to give them jobs; authorities are pumping money into the market; and AI-capital expenditures continue to surge to unprecedented levels.

And the cherry on the cake: all of these factors, combined with an expected 4.2 CPI inflation2, are enough for a 4.7 percent sell-off in precisely the sector currently contributing the most to US economic growth.

If this sounds like a very complicated and fragile Ponzi-scheme keeping the economy afloat, that is because, partially, it is. While I would love AI to provide the productivity gains that its fanatics tout, they just aren’t there yet. It would probably take robotics-based AI to make a meaningful contribution to productivity growth.

But the AI bubble is only the surface. Underneath it is a slow-motion crisis in the dollar system itself, decades in the making. This is the thing I spent my Masters thesis (capstone project, for Americans) trying to understand, and what this whole article is really about. Hold that thought.

The concerning part is that seven of the biggest tech stocks now make up around 35 percent of the entire stock market, up from barely 12 percent a decade ago. Just for context: that means a lot of retirement funds and pops and moms who bought the S&P 500 are ALL-IN on the AI-trade.

Those names are soon to be joined by a plethora of previously private companies entering the stock market — SpaceX, Anthropic, and OpenAI all intend to go public soon with a combined valuation north of $3 trillion. On top of that, Google’s parent company Alphabet is selling $80 billion dollars in stock, the largest equity capital raise ever, on top of a $30 billion-plus global bond issuance in February.

It is hard to overstate how big of a reversal that last fact is. Before AI became investable, the growth of tech-giants was decelerating. Most people had smartphones, app downloads for instagram and youtube were into the billions. The companies were actively making their products worse to earn more money.

So big-tech was basically sitting on this huge pile of money, with nowhere to spend it.

This birthed the weird moment when Mark Zuckerberg renamed Facebook to Meta and started to throw good money after bad trying to get people to live in a virtual world rather than a real one.

But more importantly, it meant these companies started to buy back their stock on a massive scale. Approximately over $1 trillion flowed back into markets through buybacks in the decade to 2024 boosting asset prices higher and higher.

The Great Reversal — from buyback-machine to CapEx-behemoth

Now, as Google and Meta both show, that flow has reversed. Tech is now draining money from the financial economy through an upcoming $3 trillion IPO-fest, selling stock, issuing bonds, and importantly, ceasing stock buybacks.

At the same time, tech is investing $400 billion into the real economy against realised AI revenue of about $100 billion, contributing to the very hot growth and inflation that will make their debt-fuelled buildout more expensive through interest rate hikes.

So what’s keeping valuations afloat (for now)? It’s a combination of two things.

First, massive hype around AI is getting people to put all of their money into tech. I was recently listening to the Forward Guidance podcast where Quinn Thompson called it “partaking in the casino”, and that is exactly what it is.

When your grandma starts telling you she “is extremely bullish on semiconductor stocks”, your bubble-o’-meter should be off the charts.

Stocks are worth what people are willing to pay for them. This shows most visibly in the forward valuation of tech (~29x earnings) relative to other less cool sectors such as utilities (~18x), consumer staples (~22x), and energy (~19x). The market is paying roughly 1.5 times as much per dollar of earnings for an AI software company as for the utilities building out the grid to power its data centres — and for the energy companies supplying the fuel.

The flip side of this compression is that capital is not flowing into sectors without a hype story to tell: money that could be going into the grid or into energy, is instead queuing up for the next AI IPO.

Second, and BY FAR the more important reason, but also the more complicated one: the US monetary and fiscal authorities are manipulating the financial market to make everything look fantastic.

Stick with the technical part that follows, because it leads somewhere genuinely alarming. There is currently a huge battle unfolding over who has power over the US economy, between the independent3 Federal Reserve and the Treasury (the executive), happening right now in plain sight — but most don’t know that it is happening.

Trump seems to be particularly obsessed with the stock market, treating it like it’s his approval rating. He’s likely constantly telling Scott Bessent to juice the books. And during war-time, that is also geopolitically important, because a crashing stock-market is not good for negotiations.

Even though Trump is arguably worse in this regard, this is also a bipartisan problem because of reasons I will explain below.

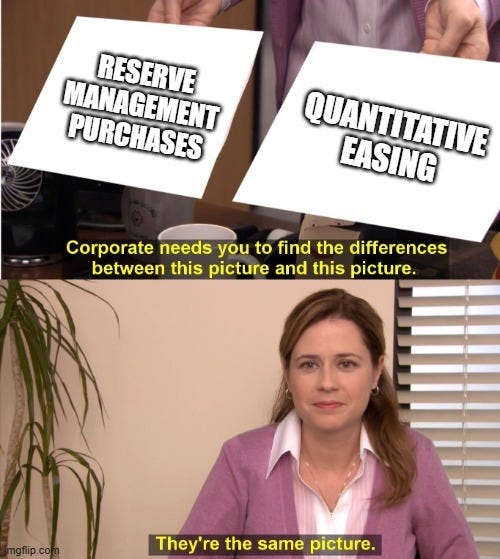

We are definitely not doing QE (yes we are)

Despite all the rhetorics coming from the Federal Reserve and those in government regarding Quantitative Tightening, the Federal Reserve and the Treasury have been flooding the financial economy with liquidity through the back door. People in mainstream media don’t tell you this because they either think you’ll find it too complicated and click away, or they are not interested in telling you the truth.

I’ll have a go at it to prove them wrong. Will you prove them wrong too?

What follows is the most technical stretch of the piece, and the most important. Stay with me through it. This is the part the specialists understand and you’re not meant to, and once it clicks, suddenly you will understand what’s happening in the US economy. Once you see it, you can’t unsee it.

Finance nerds can skip this: QE and QT — a quick glossary.

Quantitative easing (QE) is the central bank creating money to buy government bonds (debt). The immediate effect is to push investors out of those safe assets and into riskier ones such as stocks, real estate, and corporate debt (such as AI-debt) inflating their prices. The intended real-economy effect is cheaper borrowing and more lending; how much of that actually reaches ordinary people is heavily disputed. In actual fact, it seems to mostly benefit wealthy individuals who own financial assets and contribute to monetary inflation (which is different from inflation that you experience in your pocket, which is also influenced by the costs of production and productivity gains etc.), and can eventually spill over into consumer price inflation. Quantitative tightening (QT) is the opposite that has been promised by authorities: the bank stops buying, lets the bonds mature, and drains that money back out of the system.

In December 2025, the Fed officially ended quantitative tightening — having unwound only half of its pandemic-era expansion, leaving a $6.7 trillion balance sheet in place. Since then, it has been doing something that is TOTALLY not Quantitative easing, namely, “Reserve Management Purchases” in which it buys Treasury bills en masse. I’ll explain the implications in a second.

The Fed’s own FOMC minutes concede that the economic effects, namely: lower rates, higher liquidity, easier financial conditions — are similar to those of traditional QE. The Treasury has been running its own programme in parallel. It is buying back its own old bonds from banks in weekly operations of up to $4 billion, greasing dealer balance sheets and keeping credit flowing. The Treasury’s cash pile at the Federal Reserve currently sits at $845 billion.

But the most important mechanism ran for two years with barely a headline. Only the specialists are told this stuff. I’ll explain it to you in simple terms.

Remember how QE works: the Fed creating money to buy bonds. The banks it buys those bonds from get cash reserves in return. In theory they lend it out into the economy. In practice, they often just sit on it.

And it would be a shame if banks can’t do anything with the free money they just received.

So the Fed created the overnight reverse repo facility as a release valve: a place where financial institutions can hand their excess cash to the Fed at the end of each day, earn a small interest rate on it, and get it back the next morning. Money parked there is not circulating in the financial system. At its peak in 2022, over $2.5 trillion was sitting in this facility.

That is roughly the GDP of France, doing nothing.

Bills, notes and bonds — a quick distinction

US government debt comes in three forms defined by how long before it is repaid. Treasury bills mature in anything from a few days to 52 weeks. Notes mature in two to ten years. Bonds in twenty to thirty. The maturity difference determines who buys them and what happens to the money. Long-term bonds are bought by pension funds and insurance companies, who lock them away for years. When they buy, money effectively leaves short-term circulation.

Bills are bought by money market funds and banks, who hoover up these assets with alacrity, and treat them as near-cash. As investor confidence in long-term US debt sustainability frayed, demand for long-dated bonds weakened and yields on them rose. Issuing more T-bills became the path of least resistance.

Why does it matter whether that money is doing nothing? Because money loose in the financial system gets spent on financial assets, and pushes their prices up. Money frozen at the Fed does none of that. So what moved it? The US Treasury’s deficit.

Now here comes the bubble story: between 2023 and now, the ballooning fiscal deficit was being funded largely with Treasury-bills rather than longer-dated bonds. This policy started under Treasury Secretary Janet Yellen — and was heavily criticized by current Treasury Secretary Scott Bessent, who ironically has doubled down on this policy now that he is in office. It seems to be the case that they just can’t stop doing it.

Why can’t they stop doing it?

First, it is super unpopular to shrink the deficit because that would require austerity. Second, it is also economically difficult (some may say, impossible) to do for complicated reasons: such as a lack of international coordination or unilateral taxes on capital inflows, that have to do with the dollar being the reserve currency — as Michael Pettis has been arguing for years already.

Which brings us back to that $2.5 trillion sitting inert in the Fed’s parking lot.

When a money market fund parks its cash at the Fed, that money is frozen. But when the same fund uses that cash to buy a T-bill instead, it hands the money to the Treasury, which then spends it immediately on salaries, government contracts, programmes, straight into the economy.

Same cash, opposite effect. One freezes it; the other releases it. So as the Treasury started to issue trillions of dollars of T-bills, money market funds pulled their cash out of the Fed’s parking lot to buy them, and $1.96 trillion that had been sitting frozen came flooding back into the system.

This is the crucial point: none of this was a decision by the Federal Reserve. It happened because the Treasury chose to fund the deficit with short-term bills rather than long-term bonds.

Had they issued ten-year bonds instead, pension funds and insurers would have absorbed them, and the money would be locked up. But T-bills went to money market funds, which pulled the cash directly from the Fed’s holding pen.

Regime change and its relationship to the bubble: more power to the executive

The fiscal deficit, managed in a very specific way, “accidentally” acted like quantitative easing, loosening financial conditions at the exact moment the Fed claimed to be tightening them.

Notice what that means. The Federal Reserve did not decide this (though they did accomodate it). Nobody announced it, and nobody voted on it.

The Treasury is slowly trying to take over monetary policy through fiscal decisions. And the Fed, for all its press conferences and rate announcements, was not in the room — and yet still have to accomodate it. That is the shift of power this section has been building to.

Americans, listen up. The government is actively changing the locus of power in the economy from the independent Federal Reserve towards the Treasury (under control of the President). They don’t need to take control of the Fed for this, though it would certainly help.

They are finding new ways to bolster this infrastructure. The GENIUS Act — a law designed to legitimize and expand the use of stablecoins — requires issuers to back every dollar of stablecoin in circulation with approved short-term assets, of which T-bills are the primary option. Every new dollar of stablecoin issued must be matched by a dollar of Treasury bills purchased. The law, in other words, created a captive structural buyer for US government bills — one that already likely4 accounts for approximately 30 percent of T-bill demand.

None of this shows up in the headline interest rate. It is the plumbing, and arguably it matters more than the rate decisions that fill every newspaper column, because it determines not the price of money but the total volume of it available to buy financial assets.

Raising rates only changes the price of the water; this determines how much of it is in the pipes at all. And if there’s no water in the pipes, finance bros get thirsty.

Because this is not only a power-grab by the executive to fund their fiscal programmes and manipulate the market. It is also because, well, they kind of have to do it so that the system doesn’t collapse. I’ll explain why.

The Treasury basis trade

The funding markets underneath the US government are far more fragile than most people realise.

Consider the Treasury basis trade. Hedge funds exploit the tiny price gap between US government bonds and the futures contracts tied to them, a spread so small it is measured in fractions of a percent. To turn that into real money, they borrow against the bonds in the overnight repo market and lever the position up to ninety-five, sometimes ninety-eight percent. The trade now runs to roughly $1.48-1.69 trillion (depending on measurements) as of January according to Morgan Stanley, about twice the size it reached in 2020.

The problem is that because the borrowing is so short term, it is crucial that the bond market is stable. If there is too much movement in price, dealers will start to ask higher “haircuts” for lending out cash in return for Treasuries. Because if I don’t know what the price of the Treasuries will be tomorrow, why would I lend out the money at a favourable rate?

And that is why it works beautifully, right up until it doesn’t.

The moment funding tightens or those haircuts spike, the funds face margin calls, are forced to dump Treasuries all at once, and the market for US government debt — the foundation of the entire global financial system — just freezes.

That is precisely what happened in March 2020, when the Fed had to step in with hundreds of billions in emergency purchases to halt the unwind. Regulators have been warning about it for months. It was what got Donald Trump to back down from his extreme tariffs after Liberation Day, as he said the bond markets were getting a bit “yippy”. These episodes can be easily identified by looking at the MOVE-index, an index measuring bond-volatility.

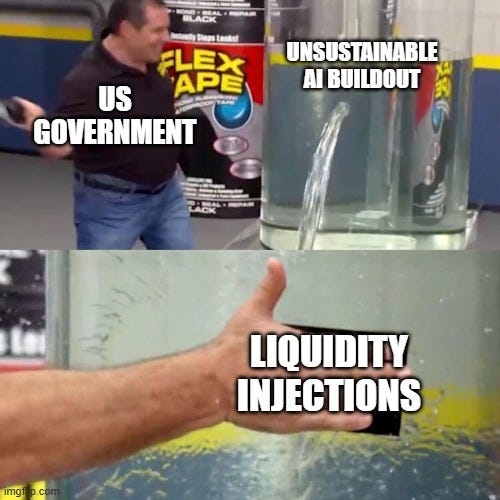

Which leaves the authorities cornered: they can talk and will talk about tightening, but financial conditions are actually loosening, because the alternative is watching the world’s safest asset go into freefall. They need to make sure there is enough liquidity in the system, otherwise bond volatility spikes.

This is especially relevant now that an incredibly large wall of debt from the 0 interest rate era is coming due, which is only going to increase in the coming years.5 This is also why policymakers are concerned about rates rising, and why Trump wants to keep rates low, because they are refinancing it with short term debt that is more vulnerable to swings in interest rates.

And this is also what’s making sure the AI-trade doesn’t collapse. Because this all keeps asset prices rising and keeps funding cheap. But then there’s the slight problem that I started this article with: it also makes the economy overheat and causes inflation.

But luckily, there’s a GENIUS in the White House. Trump admitted as much when he signed the GENIUS Act, saying “it was named after him”.

The genius in the White House

So let’s evaluate his highness’s6 policy track record: Trump decided to abandon Biden’s renewable energy ambitions, put all of his chips on fossil fuels and AI, and AFTER THAT decided to NUKE the costs of the primary input of AI: energy.

Not only that, other important commodities for the AI-buildout such as Helium, which is used in semiconductor manufacturing, and sulfuric acid which is used to produce copper that is used in data centers, are also being squeezed like a lemon.

As of Friday’s close Brent crude is currently hovering around $95-100 dollars, while WTI is hovering around $88-95, a number that is in my opinion way too low seeing the situation in Hormuz, but is likewise being manipulated by reserve drawdowns and jawboning.

Meanwhile copper is priced at $13,519 per ton on the London Metal Exchange.

The Hormuz closure put roughly a third of global seaborne fertiliser trade at risk; through April, world urea prices approximately doubled and DAP rose about 35 percent.

Urea climbed above $850/tonne in April, up 80 percent since February. Global fertiliser prices could average 15-20 percent higher in the first half of 2026 if the crisis persists. Food itself has lagged (transmission takes months): US food prices were up 3.2 percent year-on-year in April.

All of this will feed into inflation, and make the AI-trade unsustainable, that is if policymakers decide inflation should be dealt with.

So what Trump’s policy is doing, is kind of like the trick where you pull a tablecloth from the table and the cutlery stays on there, but you didn’t take into account that the real problem wasn’t the cloth, but the massive cabinet you bumped into afterwards that collapsed on top of you:

Trump has gotten himself into a sticky situation he can’t get out of, as sticky as the barnacles and other sea-debris currently multiplying daily on the hulls of ships stuck in the strait of Hormuz, causing ships to become immobile.

To summarize

So to get this straight once again, because these are A LOT of numbers: the AI-buildout is being funded by debt and the issuance of stock, which is being enabled through loose financial conditions as policymakers have been captured by fiscal problems, the AI-hyperscalers are massively short energy and commodities — and precisely those commodities are being disrupted, causing both inflation and calls for rate hikes while they just took up massive amounts of debt.

And I, as a European, cannot sit comfortably here in my chair in the Netherlands being like: “look at these Americans, they’re screwed”. Because the US economy is literally the global consumer of last resort and sustains demand for the rest of the world. This is something Trump is very upset about: namely, the US is the world’s biggest importer. But it is also a powerful tool any problem in the US, will be a problem for the world.

- YouTube")

And get this: the only thing keeping this afloat is trust in the promise of AI and massive liquidity injections by authorities into financial markets.

Are you then surprised that Western elites are panicking?

Seeing as Hormuz seems to be outside of Trump’s control, there are, in my view, only two things they can do here:

Raise rates, quit the liquidity injections, and let the whole thing implode.

Kick the can down to road until after the midterms: raise rates marginally to keep appearances up, but behind the scenes inject the market with even more money and let inflation rip.

Both of these scenarios have different implications. But both of these deserve careful study and consideration, because macro-economic chain reactions are very complex. Let me know if you’d like to see that in a future article. This theoretical part is honestly the most interesting, because it translates how an acute crisis (which is in my view, very likely coming soon) can translate into a global problem that will affect billions of people.

Additionally, all of these problems are inherited from a decades-long crisis of the dollar-system, which is currently in its final phase of exhaustion. I wrote my thesis on this. It would be a lot of work to explain all of that in understandable language. Consider donating or becoming a paid subscriber so I can help you understand our predicament better.

A closing thought: I wonder how much of this is deliberate financialized industrial policy for the new AI-manhatten project. Maybe interesting to explore in the future.

To reflect my current commitment to this publication, and the fact that I will soon be paywalling some parts of larger and more labour-intensive pieces, I will raise subscription prices to 8 euros per month and 80 annually somewhere in the next few weeks. If you enjoy my content, and would like to support me, you should subscribe now to lock in a cheaper rate.

Thank you for reading. I write this between deadlines, on my own time, without pay. If it was worth yours, buying me a coffee would mean a lot. Also consider subscribing.

Figures change drastically depending if you count self-reported or measured in terms of income. I don’t have enough time to check the methodology. But more generally, it illustrates the broader point that current growth is increasingly lop-sided, often called the “K-Shaped economy”.

Reported on Wednesday the 10th.

Some might question how independent the Fed has historically been, but the regime change is still happening.

This is extrapolated from current stablecoin market cap growth. A rough estimate. From the Paris Report: “For the time being, the overall size of the stablecoin platforms (around $280 billion) is relatively small compared to the T-bills market of $6.2 trillion, but in terms of flows, they already matter. Indeed, the platforms grew in size by about $100 billion in 2025, while net issuance of T-bills stood at $360 billion. Assuming around 80% of their reserves consist of T-bills, stablecoin platforms last year absorbed on their own between 20% and 25% of net issuance”

“The paper projects out by calendar years the maturity walls for $28.95 trillion in outstanding Treasury debt already on the books as of July 31, 2025. In 2026 alone, Mr. Campbell writes, $4.175 trillion of that debt will mature and likely will be rolled into new, higher-cost securities if the Federal Reserve by then has not brought down official short-term interest rates. “The maturity walls in 2027-2028, the remaining years of the Trump administration, likewise will roll into higher coupons absent a decline in interest rates,” Mr. Campell writes. “And this debt stock omits net new debt being issued to cover a federal deficit currently running at $1.9 trillion, or 6.5% of U.S. gross domestic product. Given this outlook, the president understandably is pressuring the Fed to lower interest rates.”

I wonder if I can still travel to the US after this. Shucks.

Nice overview and analysis. With the GENIUS & ARM act's in the works, though it's far from a sure thing if they will pass, looks like they are going with the classic option 2. Kick the can and goose, market, then try to control the narrative and manipulate the citizens into directing their pitchforks in the other direction. Ugh.

I often attempt to explain these financial machinations to my wife on our morning walks, all without sounding wonky. Still, one of the toughest things to explain is how money doesn’t exist until it is borrowed and the interest rate on borrowed money is always a problem for the lender.